Looking for something else?

Welcome

“All economic forecasts are subject to considerable uncertainty. There is always a wide range of plausible outcomes for important economic variables, including the federal funds rate.”

– Federal Reserve Chairman Jerome Powell

Rapidly shifting narratives

The first half of 2022 was marked by abrupt increases in inflation and Fed interest rate hike expectations, geopolitical shocks, soaring gasoline prices, and rapidly shifting market narratives. Both the markets and the Fed struggled to adjust to rising inflation that – while already on the upturn – spiked even higher from the impacts of the war in Ukraine. In the late spring, conventional wisdom coalesced around the economy falling into recession as a foregone conclusion. That narrative lasted a handful of weeks until both resilient consumer spending and a persistently strong labor market shifted the narrative to incorporate the possibility of a “soft landing.” More recently, market-based expectations of future inflation have moderated, commodity prices have softened, and the beginning of Q2 earnings season has seen mixed – not terrible – results. Nonetheless, there remain several major risks whose range of possible outcomes remains quite broad.

The Fed, inflation, interest rates, and fixed income markets

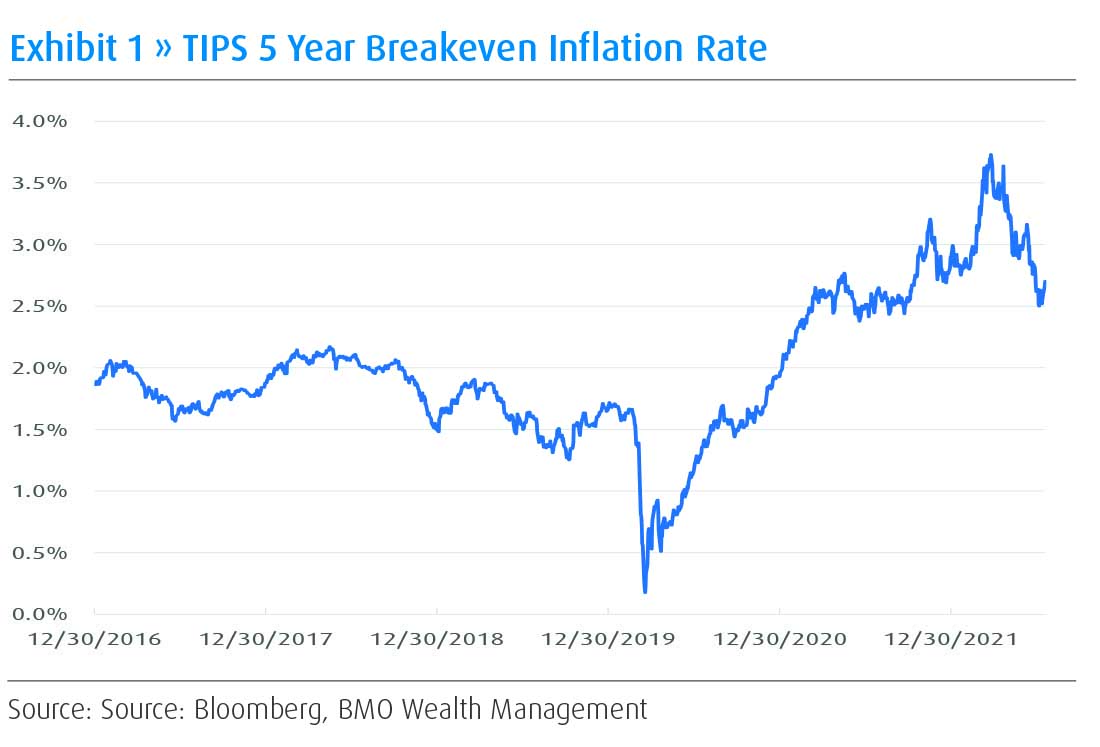

Inflation expectations have come down considerably from just a couple of months ago. The TIPS1 “breakeven inflation rate” is a market-based measure that proxies for future inflation expectations and has come down a full percentage point from its peak (Exhibit 1). The Fed is still expected to raise interest rates through year end with the short-term Fed Funds rate likely settling between 3.25% and 3.75%. Further upside inflation surprises – or even persistent inflation stickiness – would increase the possibility of excessive tightening by the Fed.

The sharp rise in interest rates earlier this year resulted in fixed income returns turning negative at the same time equities were falling. After pricing-in Fed interest rate expectations, the high quality areas of short-term fixed income now provide much more safety in the portfolio, and the high-quality areas of longer duration fixed income can better serve as a portfolio hedge in the event of further equity market selloffs.

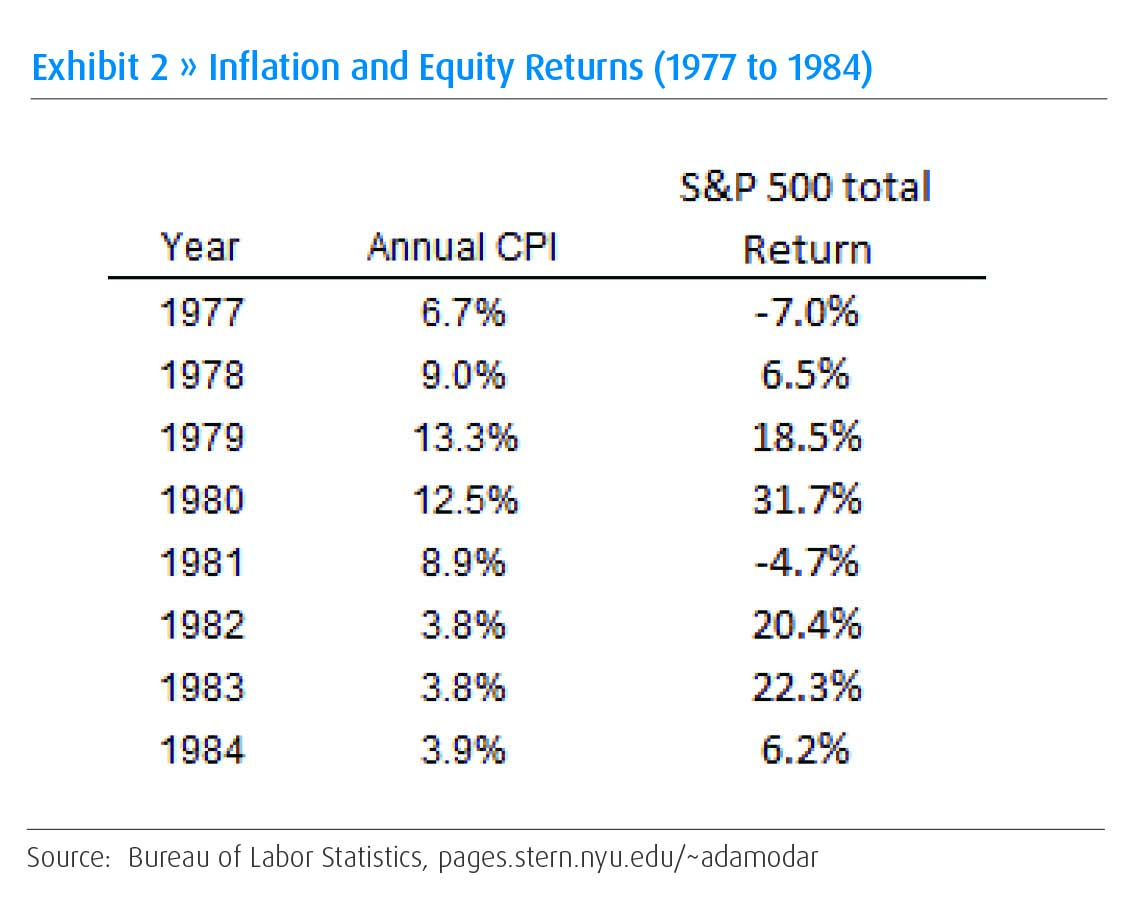

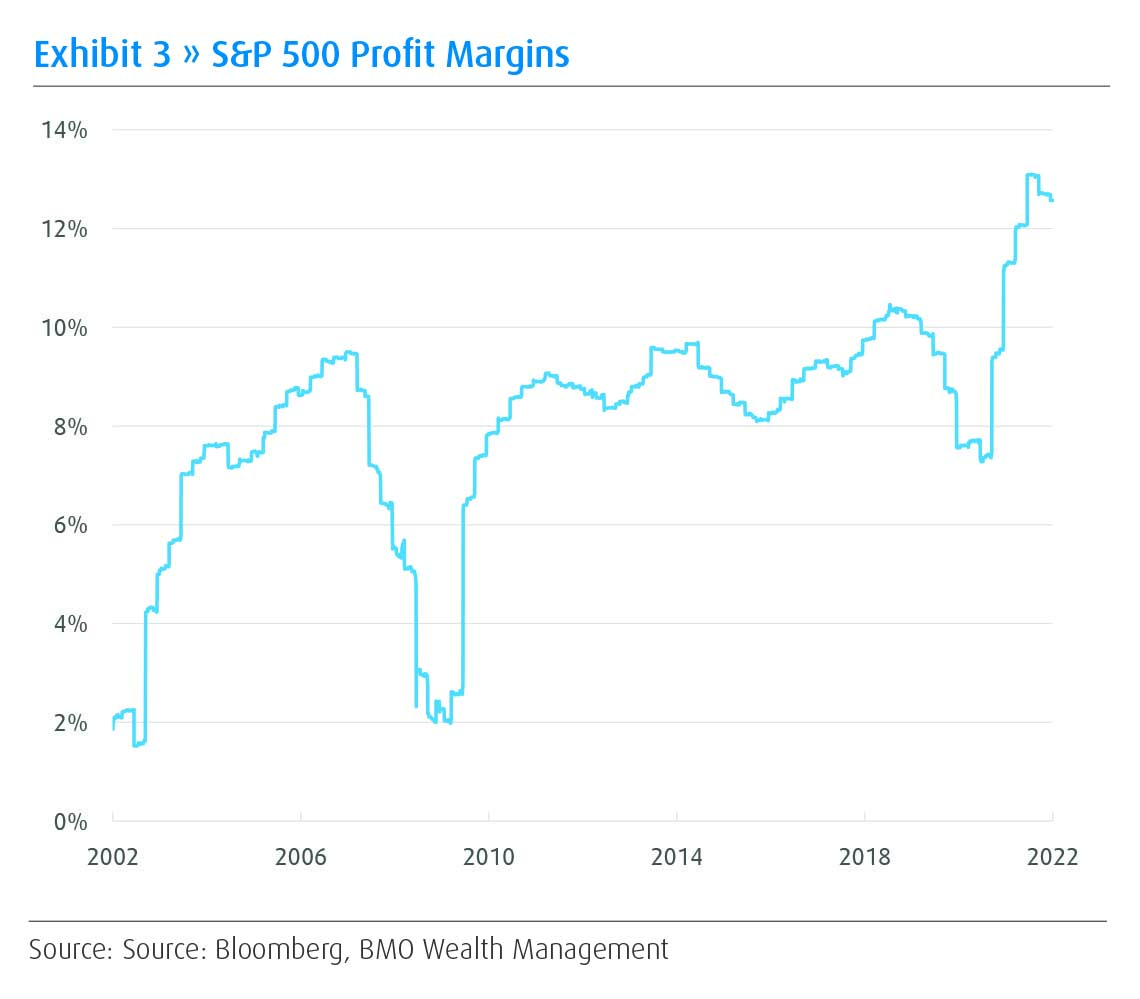

Going forward, our focus is equally – or even more so – on the expected degree of Fed tightening as it is on inflation itself. Equities can still perform reasonably well in an inflationary environment as was seen in the late 1970s and early 1980s (Exhibit 2). In many instances, companies have sufficient pricing power to raise prices and offset their own rising costs. The ongoing growth concerns, however, present the risk of drawn-out stagflation, which would clearly be negative for equity markets. On top of growth concerns, corporate profit margins are extraordinarily high on a historical basis (Exhibit 3). There are multiple reasons why profit margins have risen so much (e.g., the rise of technology megacaps and lower effective corporate taxes), but the current environment of slowing growth, high input costs, and a tight labor market increases the risk of profit margin pullback.

Recession or no recession?

We can propose a recession probability, but we believe the more appropriate question is “soft landing” or “hard landing”? Growth has slowed; that is already baked in. Whether growth has slowed just enough to stay out of what the official National Bureau of Economic Research recession dating committee decides (retroactively) is a recession is not a primary consideration. A “hard landing” would be an entirely different story altogether – that would be marked by an even steeper slowdown and sharply declining corporate profits. We continue to believe the prospects for a hard landing are lower than those of a soft landing, and the greatest risk for a hard landing is Fed over-tightening.

On the positive side, in aggregate, both households and corporations have low leverage, high savings, and low debt servicing requirements. In the 2001 and 2008 recessions, there were substantial amounts of misallocated capital and leverage that resulted in a negative feedback loop when the economy slowed. The current economic environment may still have areas of froth – cryptocurrency, SPACs, and pre-IPO tech “unicorns” come to mind – but these do not appear to have the far-reaching economic implications of prior economic distortions. The current relatively stable economic underpinnings are supported by a labor market that remains healthy and steadies consumer spending. Strains are emerging, but the lack of major imbalances should allow for “bend but don’t break.”

The U.S. housing market

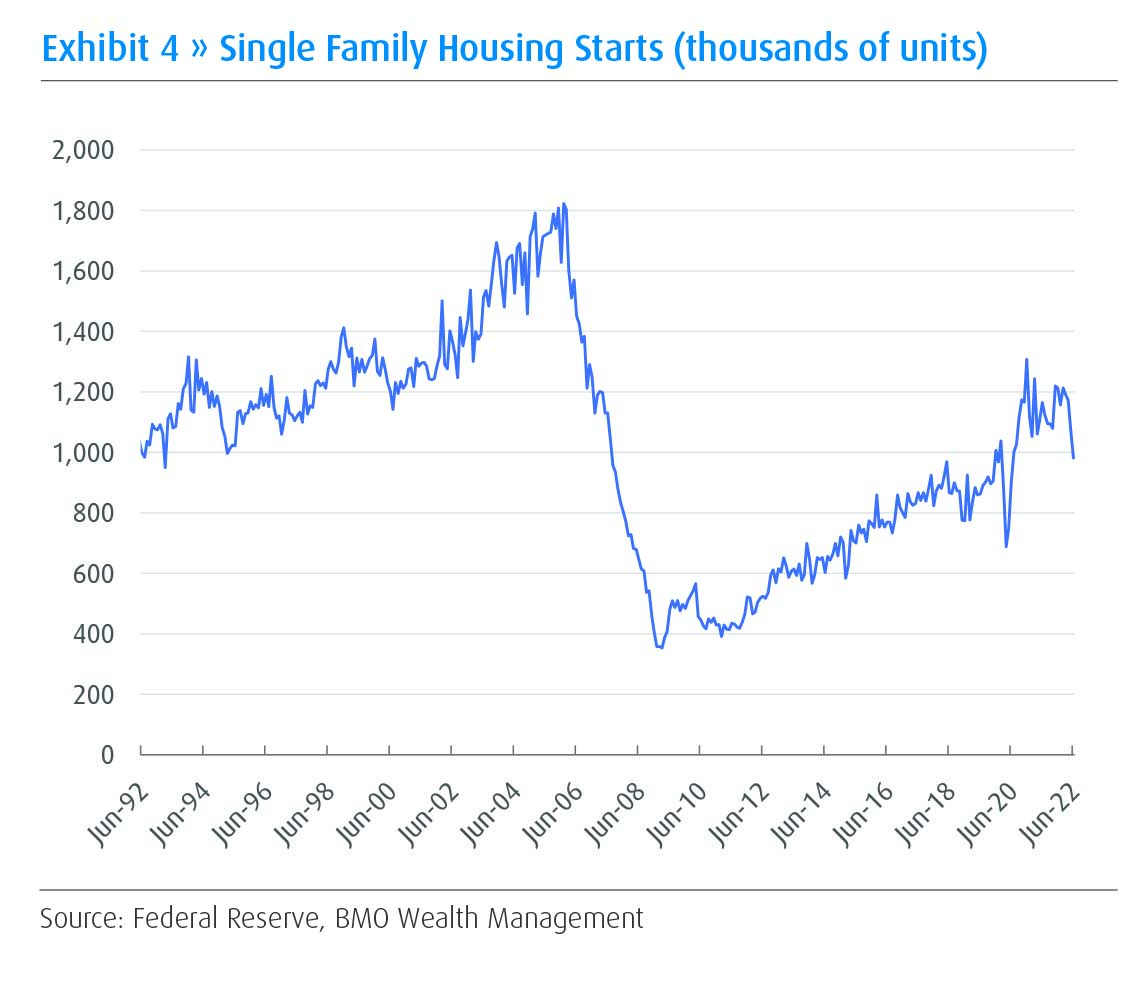

The housing market is clearly pulling back due to the combined effects of high prices and rising mortgage rates that have strained affordability. Homebuilders are reporting falling demand and housing starts have fallen to a 2-year low (Exhibit 4). This housing downturn, however, is likely to be short lived. From 2012 through 2021, over 12 million households were formed in the U.S. but only 7 million new single-family homes were built during that time2. The accompanying graph indicates the decade-plus dearth of home construction that has finally caught up with us. Given this medium-term supply-demand dynamic, we expect home sales to slow sharply for a few quarters and prices could fall modestly, but we expect stability and balance should emerge in the housing market again by the spring of 2023.

Midterm U.S. elections

Pundits and prediction markets are giving high odds to Republicans regaining control of the House. Control of the Senate, however, is a closer call. Any outcome other than one-party control of the White House and both houses of Congress implies gridlock on major issues such as taxes and fiscal spending which have more market-moving implications. The near-term market impact of the midterm elections is therefore likely to be modest. The midterms may raise the stakes for the 2024 Presidential election, but there are far too many considerations presently in play for the markets to worry about an even more uncertain division of power that is two years away.

Geopolitics and international markets

We continue to recommend an underweight to both international developed equities and emerging market equities. The trajectory of the war in Ukraine, Europe’s and America’s response, and the economic warfare have continued to surprise geopolitical prognosticators and the markets in general. What was expected to be a quick Russian victory with little economic response from Europe has turned into a drawn-out war with sophisticated weapons being supplied by the West. Economic sanctions, initially off the table, soon came forcefully from the U.S. and Europe. Not to be outdone, Russia raised the stakes by reducing – and potentially cutting off – the flow of natural gas to Europe, which could lead to crippling effects on European industry. In short, risk in Europe remains elevated. Europe faces slowing growth and high inflation, but also greater geopolitical risks. The endgame for the war and its economic impacts are still very uncertain.

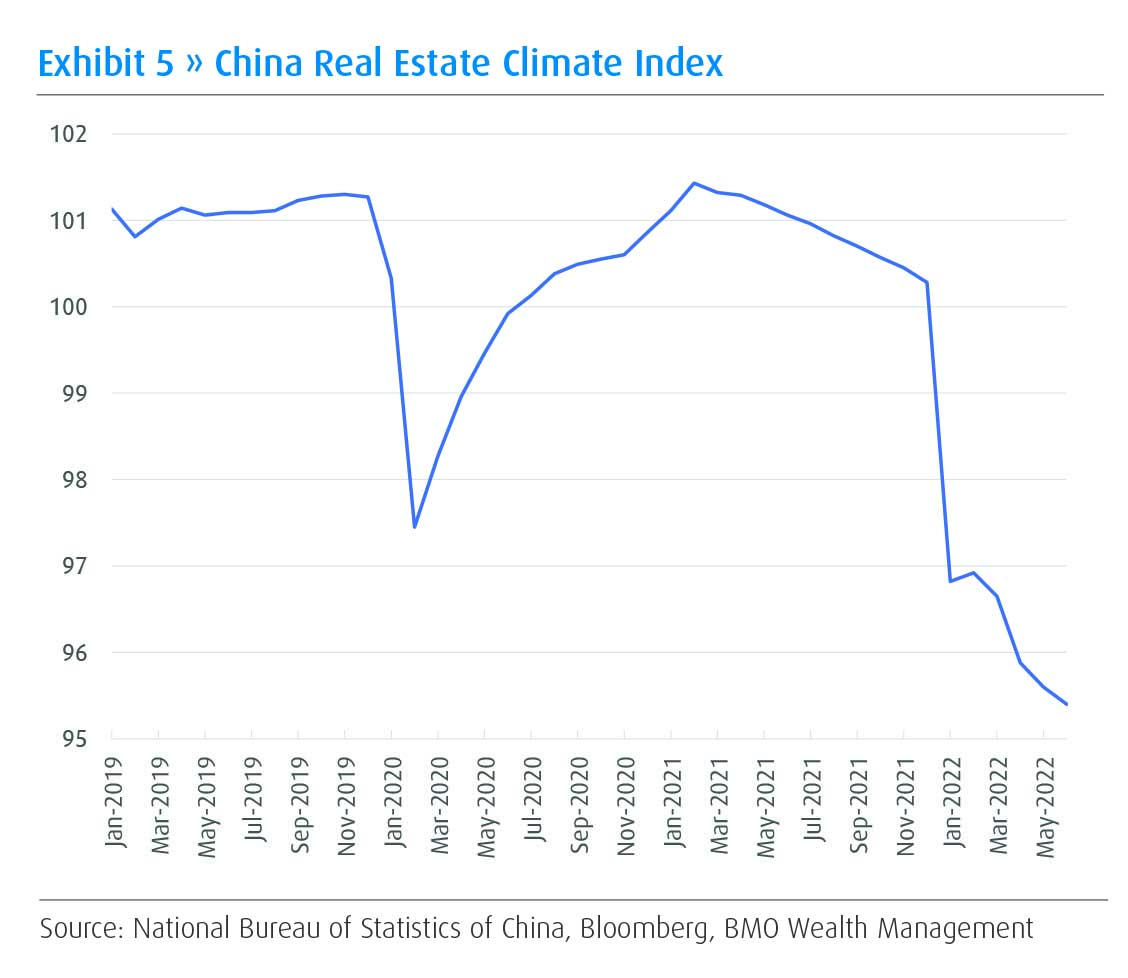

Our recommended underweight to emerging market equities remains in effect and was initiated based on the belief that China’s property model is broken. Those property sector risks continue to play out (Exhibit 5) and we do not see a quick path to stabilization. The outsized contribution to GDP and composition of household wealth that housing constitutes in China point to significant risk. Aggressive Covid lockdowns in China add to the country’s economic challenges, although we expect those lockdowns to begin easing by year end. Overall, while equity prices have come down in international markets, risk remains elevated and not adequately compensated by the range of likely outcomes.

Portfolio approach amid heightened uncertainty

Our recent portfolio recommendations have focused on reducing equity risk – both international and U.S. – and increasing portfolio stability through high-quality, short-duration fixed income. Earlier recommendations also included reducing certain areas of international risk and adding small diversifying positions in publicly traded real estate and commodities. Such positions don’t always provide the desired diversification as the recent few months have shown, but they do increase the likelihood that portfolios will be better positioned overall to withstand various environments.

Both equity market and fixed income market valuations are best described as “neutral,” which points toward a balanced approach across those asset classes. Additionally, our proprietary BMO Sentiment Metric shows a very high level of investor pessimism. As a contrarian indicator, this tends to play out favorably for equity investors over the ensuing 12 months. A statistical regularity, however, is still not an assurance and each cycle can have its own dynamics.

The multiple risks we have outlined do not need “resolution”, per se, for the equity markets to regain their footing. In what remains of 2022, we are on the lookout for the path of these major risk factors – inflation, Fed intentions, profit margins, economic conditions, and multiple international risks – to narrow in the direction of market-digestible trajectories. At present, risk and uncertainty remain elevated and there is a wide dispersion of possible outcomes and combinations. Until those trajectories come better into focus, we expect that ongoing portfolio shifts would continue to lean toward greater diversification and stability rather than greater risk taking.

___________________________

1 Treasury Inflation Protected Securities (TIPS), whose par value adjusts based on the inflation rate

2 www.cnbc.com/2021/09/14/america-is-short-more-than-5-million-homes-study-says.html

Stay on top of the latest news and insights from BMO Wealth Management