Looking for something else?

Welcome

Fitch, one of the three major credit rating agencies, downgraded U.S. debt on August 1st from AAA to AA+ citing “expected fiscal deterioration over the next three years, a high and growing general government debt burden, and the erosion of governance.”1 Following the announcement, U.S. and global equity markets had a challenging day, with major markets falling over 1%. This stock market reaction, at least so far, has been mild in comparison to the equity market spasm back in 2011 when another rating agency, Standard and Poor’s, made the initial downgrade of U.S. government debt.

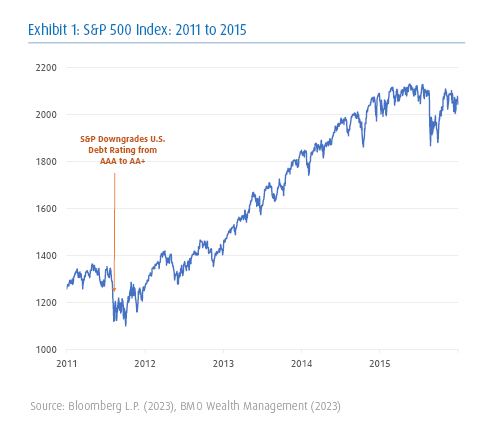

The market environment back in 2011, however, was very different than today. While the stock market had clearly bottomed from the Great Financial Crisis lows, ongoing concerns of a European debt crisis and a shocking debt ceiling standoff weakened the underpinnings of the equity market. In 2011, the bout of market choppiness lasted for months, but by 2012 the S&P 500 was again making new highs and never looked back (Exhibit 1).

Recently, equity market performance has been strong, inflation has clearly moderated, the Fed’s rate hike cycle is (hopefully) coming to an end, and the labor market remains healthy. We continue to recommend a balanced approach to risk as the soft-landing takes shape.

It is important to keep in mind, however, that the Fed’s interest rate increases have yet to ripple fully through the economy, and we expect the economy to slow in the coming months. In that context, the rating downgrade is unhelpful and risks denting investors’ risk appetite. The debt downgrade by Fitch does not change our general outlook, but it does draw attention to the U.S. fiscal position that will likely turn into a headwind in the coming years as the interest burden to service government debt continues to grow.

__________________

270.9 KB PDF

270.9 KB PDF

Stay on top of the latest news and insights from BMO Wealth Management