Looking for something else?

Welcome

Traveling to warmer climates for the winter is a tradition for many families, as is taking advantage of southern states with lower, or no, income taxes. Increasing interest in changing domicile — the location of a person’s fixed, principal and permanent home — to select the best state for tax purposes is becoming more common.

Interest in changing domicile for tax reasons began to accelerate about 20 years ago due to tax law revisions made by the Economic Growth and Tax Relief Reconciliation Act of 2001 and the real estate bubble that occurred in the following years. More recently, the COVID-19 pandemic has made working remotely the new “norm,” allowing individuals from high-income-tax states, like California and New York, to make a permanent move to no-income-tax states, like Florida, Nevada, and Texas. And as high-income-tax states continue to propose increasing taxes to deal with budget deficits that have been exacerbated by COVID-19 pandemic shutdowns, lower-, or no-income-tax states are becoming more attractive.

Let’s take a closer look at domicile, the consequences of changing it, and recommended steps for making a permanent move.

Domicile is the location of a person’s fixed, principal, and permanent home, and the place to which that person intends to return and remain, even if currently residing elsewhere. Domicile is different from residency. While a person can have multiple residences, a person can only have one true domicile. For example, a person can reside in State A, but still be considered domiciled in State B, if the stay in State A is temporary and the intent is to return to and remain in State B.

States, especially the taxing authority of each state, will look at a number of elements to determine domicile. The factors considered will differ from state to state, and no one factor is completely determinative.

Relevant factors state taxing authorities may consider in determining domicile include:

Once domicile is established, it is presumed to continue until it can be shown that a change in domicile has occurred. Termination of domicile will involve documenting the change to a new domicile and may require communicating the change to the appropriate state’s taxing authority, which can sometimes be more difficult to prove than establishing a new domicile.

Property ownership rules are governed by domicile. Laws of the state in which you are domiciled will determine your right to retain, manage, and transfer property and the rights of others to make a claim on your property. States may also impose taxes on a person domiciled in their state. From a planning perspective, state taxes—including income, property, sales, and death taxes—are probably the most important aspects to consider when selecting domicile. Asset protection and the rights of a spouse in the event of divorce may also be important considerations.

The laws apply depending on your place of domicile. The impacts of the laws may change depending on a person’s age, amount of income, type of income, size of estate, and home value. The following state taxes are important to consider when selecting your domicile.

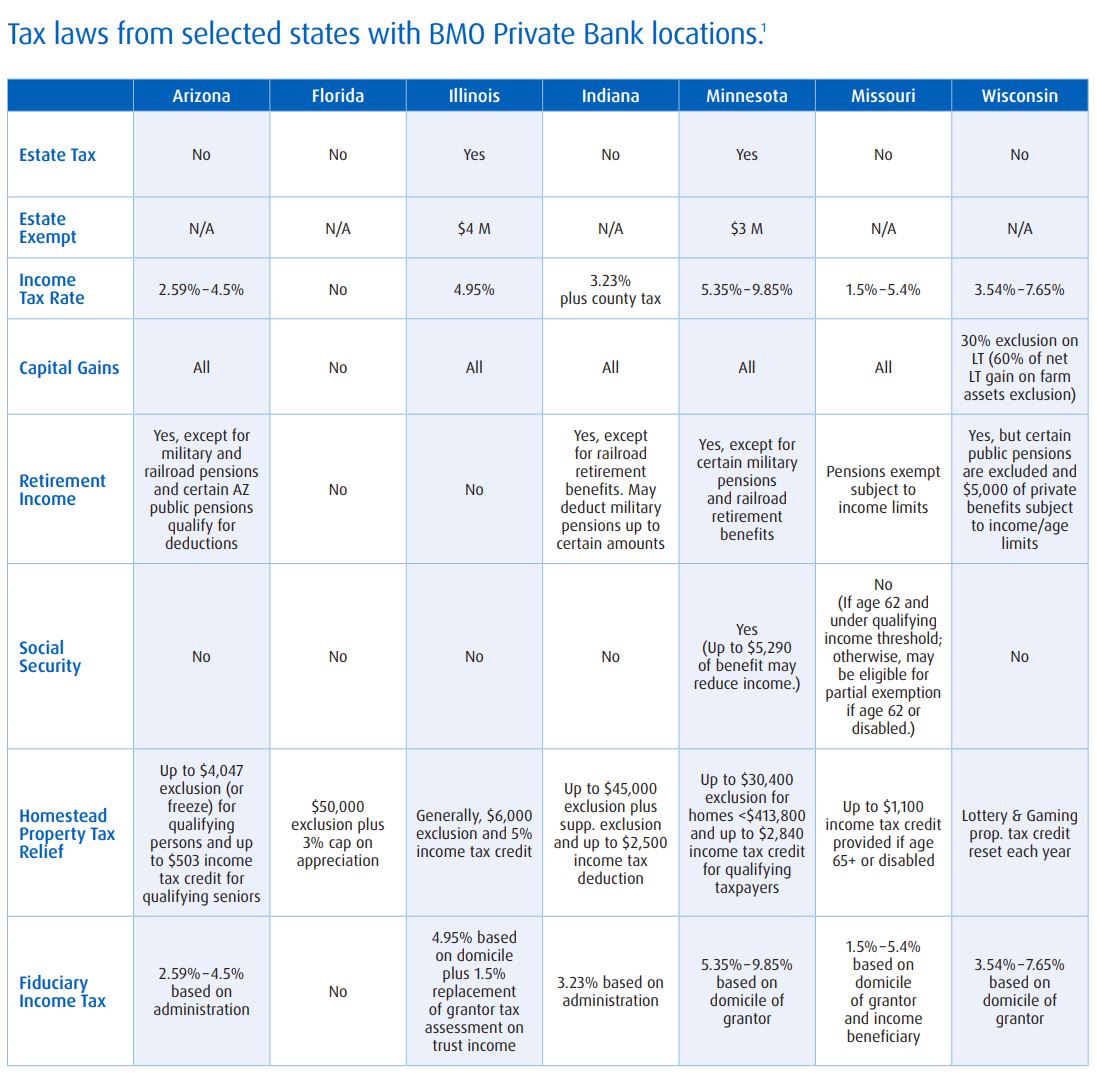

Income taxes. Selecting domicile in states like Florida, Nevada, or Texas, that impose no income tax can be an effective tax reduction strategy. However, a state can tax a non-resident on income that is earned in that state. This includes compensation earned in that particular state (wages, salary, deferred income, Subchapter S income, and income from a partnership or LLC), and income earned from a state source (such as rental income or capital gains when real estate located in that state is sold). Thus, keep in mind that even if you effectively change your domicile to State A, which is a no-income-tax state, but continue to work in State B, which taxes income, you will not necessarily avoid income taxes on your earned income.

Also keep in mind that prior to the 2017 Tax Cuts and Jobs Act (“TCJA”), taxpayers were allowed an unlimited deduction on their federal income tax returns for state and local taxes (“SALT”) paid. This was a big incentive for homeowners in high-property-tax states. But under the TCJA, SALT deductions for tax years 2018 through 2025 have been limited to $10,000 for single taxpayers and married couples filing jointly, thereby removing the tax incentive to remain domiciled in a high property tax state.

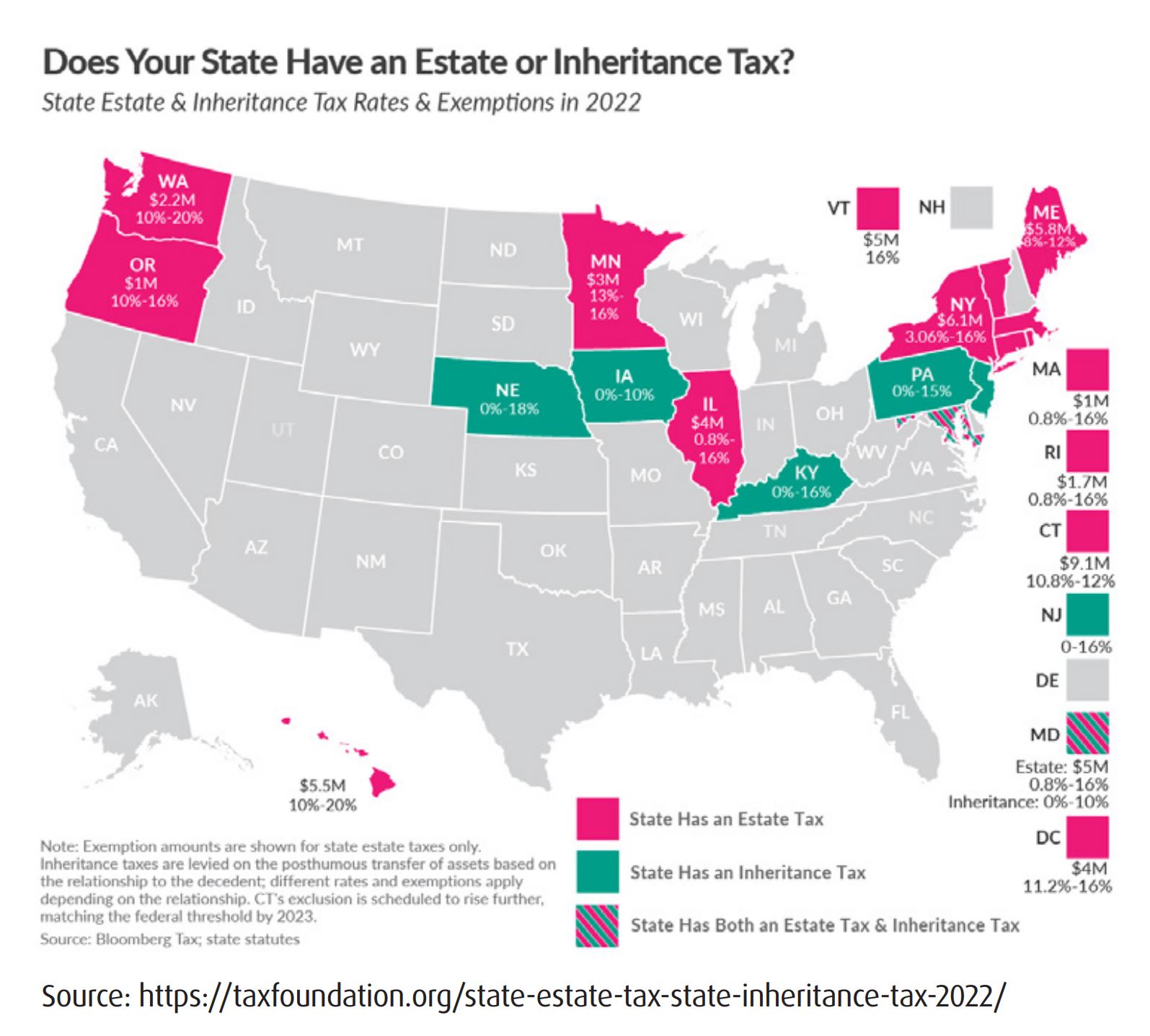

State death taxes. Planning to minimize state death taxes is simple — except for owning real property located in another state, you avoid a state death tax if you change your domicile to a state that does not impose such a tax. States that do collect an estate or inheritance tax will generally impose the tax when a person domiciled in that state dies, or when a non-resident dies owning real property located within that state.

Real estate taxes. Most states give their residents a tax break if a home is used as a principal residence. Typically, this relief is in the form of a reduction in the assessed value of the home, a credit against property taxes owed, or a state income tax credit. If you decide to change your domicile, it will be important to notify your current property tax assessor that you have moved and are no longer eligible for any homeowner tax relief. Otherwise, you may face significant taxes, interest, and penalties if you are “caught” claiming two primary residences.

Fiduciary income taxes. Fiduciary income taxes — taxes imposed on certain estates and trusts — apply in states that impose a state income tax at rates similar to the individual state income tax rates. Fiduciary income taxes often apply to trusts that become irrevocable when the creator of the trust (the “grantor”) is domiciled in the state. Frequently, the event that causes a trust to become irrevocable is the death of the grantor. Thus, to avoid fiduciary state income taxes, it may be advisable to change your domicile to a state without fiduciary income taxes before your trust becomes irrevocable.

[Note: Some states impose a fiduciary income tax on irrevocable trusts that are administered in that state.

Aside from imposing no state income taxes (personal or fiduciary) and no state death taxes, Florida has taken on heightened domicile interest due to its generous property tax breaks. Back in 1995, Florida amended its laws to impose a cap on increases in the assessed value of property that is used as a primary residence, referred to as a “homestead.” The Florida “Save Our Homes” property tax amendment imposes a cap on property appreciation assessments for a homestead equal to the lesser of 3% or the increase in the Consumer Price Index over the prior year. As a result, when the real estate bubble in the 2000s caused an annual increase in Florida property values from 8% to 27%, Florida real estate tax bills for similar properties varied significantly based on whether the property was a homestead, and this continues today.

Florida amended its property tax laws again in 2008 to further differentiate between homestead and non-homestead property by increasing the homestead exemption from $25,000 to $50,000. In addition, when a homestead is sold, its untaxed appreciation may be transferred to a new Florida homestead (subject to a cap). Finally, the non-homestead annual increase in property taxes was changed from an unlimited amount to a cap of 10%.

A Florida real estate tax case study. A Florida real estate tax case study. Two neighbors purchase identical condos for $500,000 in Coral Gables in 2022. One is not domiciled in Florida and the other is domiciled in Florida and receives the homestead exemption. Per the Miami-Dade Property Appraiser Tax Estimator (https://www.miamidade.gov/Apps/PA/PAOnlineTools/ Taxes/TaxEstimator.aspx), in 2022 the non-homestead property taxes were about $9,148 and the homesteaded property taxes were about $8,398. Each year this gap will continue to increase since the non-homesteaded property will receive the 10% cap on assessment increases while the homesteaded property will receive the 3% cap.

Before picking up and moving your domicile to save on state taxes, there are several details to be aware of that will impact the legal rights of you, your spouse, and your heirs.

Common law vs. community property rights and step-up in basis. The majority of states apply common law property ownership, meaning each spouse owns what is titled in the spouse’s name. On the other hand, nine states — Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin — apply community property ownership, meaning each spouse owns a 50% interest in the community property asset. Aside from this, in the past several years a handful of states — Alaska, Florida, Kentucky, South Dakota, and Tennessee — have passed “opt in” community property laws.

A benefit of community property ownership is that all assets classified as community property will receive a full step-up in basis upon the death of each spouse. This may affect capital gains tax exposure and is a reason why many people moving from a community property state to a common law property state may want to preserve the community property classification.

Split domicile. In limited circumstances it may be possible for you and your spouse to claim domicile in two different states. For example, if you and your spouse own homes in Florida and New York and you have retired and are spending the majority of your time on a Florida beach, but your spouse is still working and residing in New York, then you may be able to claim domicile in Florida, but your spouse will remain domiciled in New York. However, as already mentioned, the laws governing domicile are complex and vary significantly from state to state, so if you think you and your spouse may qualify for split domicile, it will be important to work with a knowledgeable attorney or tax advisor who can guide you through the process for effectively filing as a split couple.

Estate planning documents. Your estate planning documents should be reviewed by an attorney in the state to which you intend to change, or have changed, your domicile since these documents are governed by state laws which can alter, or even invalidate, dispositive and other provisions. It is recommended that a financial power of attorney and advance healthcare directive be prepared in the new state of domicile. You may also need to sign a new Last Will and Testament or Codicil to incorporate your new state’s laws. And since the rules governing trusts can vary significantly from state to state, if you created any trusts as part of your estate plan, a review of the trust agreements is warranted to determine if your change in domicile has affected any of the terms of the trusts.

Asset protection rights. Asset protection for your home and investments also varies significantly from state to state. If you are concerned about asset protection, then you will want to verify the impact a change in domicile will have on the creditor protection for your home and other assets.

Family law rights. Another area for consideration is the impact of a change in domicile on family rights. While a discussion of family law rights is beyond the scope of this article, if you executed a premarital or post-marital property agreement, you will want to have that agreement reviewed and possibly updated due to your change in domicile.

Depending on the state from which you are moving, the state department of revenue will likely scrutinize your move to the highest degree. In fact, many states are bolstering their department of revenue staff to monitor changes in domicile since “catching” someone who has not effectively changed their domicile can lead to significant state revenues. Therefore, we recommend working closely with your tax and financial advisors and your attorney to consider all ramifications a change in domicile will have on you and your family, and, if warranted, taking the necessary steps and precautions that will ensure an effective change.

Remember:

As you can see, changing your domicile can be complex, and becomes more so if you own homes in multiple states or you and your spouse disagree about where to live. And while a change in domicile may significantly benefit your financial situation, unfortunately there is no magic rule to prove the change. You can contact your BMO Wealth Management professional for more information. www.bmowealthmanagement.com

Stay on top of the latest news and insights from BMO Wealth Management